Excited to roll out this infographic based on Prof. Jamie Hopkins article of Forbes. Feel free to use it for your website if you are another insurance professional. Code is available below the infographic.

If you are looking for HO6 Insurance, also known as Condo Insurance, in Bel Air, Harford County, or elsewhere in Maryland, then this will be a great article to quickly review.

Consider bundling your HO6 condo insurance with your auto insurance

The bundled discount can range from 5%-25%

The ease of use for you (because you only need one company)

Get a copy of the master policy

Present this to your insurance professional

Your condo insurance policy needs to fill in the gaps the master doesn’t cover

Consider how much content coverage you need

Personal property coverage is to protect what you own that is in the condo

An easy way to take inventory is to take photos (not full-proof, but better than nothing)

Liability coverage for HO6, how much?

Liability coverage protects you in the case of a lawsuit

Tally your total assets; investments, cash, wage potential, and take that into consideration

Here is a medium article I wrote on protecting your wealth

Okay this is a big deal if you live in a condo and are considering your insurance coverage. What happens if sewage backs up through your toilet or sink? You need this endorsement on your policy for any coverage. It is a big deal that can get forgotten.

I have seen situations locally where tenants or owners on the third story put a lot of grease down the drain. This clogged the drains for the lower inhabitants and a massive back up occurred.

Definitely consider this insurance coverage for your policy.

The Price

Of course, price varies from company to company. When we lived in our condo we enjoyed coverage through Nationwide. National company with great customer service. We paid around $650/year and we had good coverage. Don’t stick me to that price – because prices changes constantly.

Here are some good condo insurance companies to work:

Travelers

Safeco

Mutual Benefit

Nationwide

They all have different rating structures and endorsements. There is a lot of standardization in the insurance industry but there is also a lot of customization between carriers too. That is the advantage of working with an insurance broker – they help you navigate it all.

I’m currently reading The Demolished Man by Alfred Bester. The first ever Hugo Award Winning novel! Very cool

I wrote up an article on Medium relating this story to protecting yourself with insurance: https://medium.com/@jessecunninghamv/protect-your-wealth-a-science-fiction-example-ebf0974135a1

It is a far leap – but I hope it serves to illustrate how we need to use insurance to protect our wealth.

Great question. Why would anyone ever need life insurance? I often get this question from single people, but sometimes from married folks as well. I wanted to write this article to discuss some different things to consider with life insurance. The purpose is to educate you on what life insurance can and cannot do. At the end of it all, then you can decide if there is any point for you to have life insurance. Because remember, everyone’s situation is different and there is never a cookie-cutter solution.

Life Insurance in a Nutshell

At the most base level, life insurance is an agreement between a insurance carrier and an individual. Both parties come to some agreement on the premium amount monthly and the death benefit if the individual were to die. Very simple right? Lets keep it simple because I don’t think it needs to be complicated, at all.

The premium is a fancy word for monthly price. Usually the policy has a level monthly price, but of course there are exceptions.

Okay now, lets build upon that agreement. The individual pays the insurance company a set premium for a set term (a specific amount of time in the contract). If the person passes away during that term then the death benefit pays to the beneficiary – tax free.

The beneficiary is the person receiving the benefit from the life insurance company if the individual passes away within the contract term.

I wanted to reiterate that the death benefit, which is the amount that the companies pays the beneficiary, is paid out tax-free. This is VERY important to remember throughout our discussion.

The big “so-what” of the matter is that a person can insure themselves for hundreds of thousands of dollars for minimal monthly outlay. This is what financial advisers refer to as leverage.

Think about it, I had a 28 year old father call me this past week. He wants to insure himself for around $500,000 of death benefit. We talked about a few options and it seems like a term plus policy (which we can talk about later) is a good fit for now. That policy would cost him between $20-$40/month!

I want to get something straight, right off the bat. If this father were to purchase this policy, pay the premium, be eligible, and pass away the next day, then the WHOLE $500,000 TAX FREE would pay to his beneficiary, which is most likely his wife.

So remember that story if you are in a similar situation. We often purchase insurance for things that may or may not happen, and hopefully he outlives the term of the life insurance policy, BUT if he doesn’t then his wife and daughter and debt-free and can focus on what matters.

Term Life Insurance

This is one of the most basic types of life insurance. Term Life. I’m sure you’ve heard of it. It is affordable, effective, and if properly designed – it can even give you options in the future.

So here it is, term life insurance is an agreement set for a predetermined term. Often it is a 10, 20, or 30 year life insurance term. If the insured dies during the term – then the death benefit will pay to the beneficiary. Very simple.

Where it becomes very powerful is utilizing it for temporary needs such as a mortgage or other timed debts.

Oh yeah, remember I mentioned that it also can give you options for the future if designed properly? Yep, very easy, add what is called a guaranteed insurability rider to the policy and it will give you many options towards other policies. We can get into that now.

Permanent Life Insurance

Very different then a term life insurance policy, PERMANENT life insurance has a set illustration, or schedule, which usually lasts to age 120. We consider this permanent because, I don’t think anyone has lived past that age.

So what is the point of permanent life insurance? There are many – so let’s see how many I can intelligibly write about without getting tired.

Permanent Life Insurance lasts your whole life

It has many more options than term life

It has the potential for cash value build up within the policy

That cash value can be accessed as a tax-free income flow if done properly

The point is that permanent life insurance is almost endless in its approach. Life insurance companies continue to improve their offerings, with new riders, and endorsements, to out-wit their competitors, all to the advantage of the consumer. Lets jump into some of those riders and endorsements now.

Riders and Endorsements

A rider, or endorsement, is an addition to a life insurance policy. They are optional coverage that enhance and change the behavior of the policy. So remember we discussed term life insurance as being the most basic, well it becomes very complex when you start to consider these riders. And please note that riders can be added to any kind of life insurance policy, for the most part. So lets discuss specific riders.

Waiver of Premium for Disability

If you get disabled, and each carrier has different definitions, then this rider will allow you to stop making your monthly premium payment. The life insurance company will technically pay the premium for you.

This rider becomes very alluring when coupled with a permanent policy such as an indexed universal life insurance policy. If someone is purposefully super funding a life insurance policy (we can get into this in another article) then the premium is high and they are doing this to create high cash value. If they get disabled per the definitions of the policy, then that super funded plan continues on, often to age 65. WOW! That changes the game when coupled with a true disability policy. MASSIVE leverage.

If you are deemed terminally ill by a medical professional, then this rider allows you to access a portion of the death benefit while you are alive. Disclaimer: every carrier has different definitions of terminally ill. Some say 12 months to live while other 24. It all depends, but that is why you should rely on your insurance professional to guide you.

Chronic Illness Rider

This is a SHINING STAR in my opinion. If you cannot perform a certain portion of the activities of daily living, then this rider allows you to access a portion of your death benefit while you are alive. This rider is usually reserved for permanent policies such as whole life or universal life insurance policies.

It is similar to a Long Term Care policy but it does have differences. It allows the insured to have some protection in case of of a long term care event. BIG DEAL.

Closing Remarks

This was definitely not an exhaustive list, quiet frankly, I just got tired and need to take a break for a bit. Hopefully you can see that life insurance has many purposes with many different configurations.

Like I stated in the beginning, there is not one cookie-cutter solution for all. There are enough riders and endorsements and different types of policies to create an almost endless variation of life insurance polices. What makes the difference is an insurance professional that cares and is knowledge.

The 15 Best Ways to Save Money on Insurance. Here is a quick list for you to consider when purchasing or changing insurance policies.

Seek out multiple quotes when considering switching to a different insurance carrier. We are independent brokers and represent many different insurance companies to find the best fit.

Audit your coverage to make sure it is appropriate. Oftentimes homeowners insurance coverage A (which is the dwelling coverage) goes up over time. If you have had the same insurance company for a long time then this coverage can creep up on you.

Bundle your auto, home, and umbrella policies with one carrier. This bundled discount is often a huge discount relative to what is available. Always bundle if possible. Some companies like, Nationwide, will even give a bundled discount if you have life insurance with them too.

Carry higher deductibles if you are able to “self insure” and pay the higher amount if a claim arises. This helps lower your monthly premiums.

Stay with your insurance company for 3-5 years before switching. Other carriers look upon this favorably when you seek out quotes.

Have good credit. This is a factor often rated for in car insurance. Some car insurance companies refer to is as an “ISO” score which is heavily based upon credit.

Consider driving monitoring programs through the insurance carrier. The insurance companies will often have a plug-in device or an app on your phone you can download that allows them to monitor how you drive. The savings can be huge.

Carry higher liability limits. This pertains to car insurance. When you shop for car insurance one of the larger rating considerations is your previous liability limits. The higher the better.

Be accident free. This is obvious but it needed to make the list. Have a clean record and you will save money.

Get an insurance quotebefore purchasing a new car. Oftentimes we see people purchase a new car without considering the insurance price. If you are going to purchase a car you can always call and get a quote to get an idea of your “all in price”.

Consider liability only on older vehicles. This is a judgement call for the owner of the vehicle – but if the vehicle is older and you can “self insure” it against a loss – then you can save money by not having comprehensive and collision coverage.

Research which cars are safe. The safest cars usually have good statistics on insurance frequency therefore a good relative insurance premium.

Notify your insurance professional of changes. If a young driver of the household leaves and now lives somewhere else it is important to notify your insurance company. Huge savings here.

Shop your insurance 3 years after an accident. This is important to do because 3 years is the usual “fall-off” date.

Work with an insurance broker. I am a little biased on this last one because I am a independent insurance broker. But it does allow us to seek out many solutions for our clients which often means savings.

I hope you enjoyed this blog post. My goal was to give you some easily digestible tips to save money on your insurance. I’m a big believer that insurance does not need to be complicated and hopefully we can educate more people on different topics.

If you would like a free quote, consultation, or review please reach out to us at 4102623176 or fill out the form below.

The latest craze going around Facebook and other media outlets – Root Car Insurance. The concept is fairly simple on the surface: download the app, root monitors how you drive, and eventually it will dictate a monthly price for your car insurance. Disclaimer: we do not offer Root Car Insurance. We are just making observations and opinions in this blog article.

Their website highlights “simple pricing, fair rates, and modern products”. As a insurance professional it is important to stay ahead of trends and understand the ever changing marketplace. I do believe there will be major disruption in the industry as time goes on, but is Root Car Insurance it? Let’s dive into some specifics of their offers before we make an opinion.

The first step to working with Root Car Insurance is to download their app on either the iPhone or Android. It is compatible with both operating systems which is very convenient. Currently the app is available on iPhone 5s and above and “most” androids.

2. Drive!

Once you have downloaded the application then its time to drive. They will monitor your driving behavior such as speed, braking, what time of the day you drive, where you drive, etc. This is not a new phenomenon in the insurance industry as the majority of insurance companies now offer plug-in devices or apps to just this.

3. Choose your plan

After a sufficient amount of data has been collected on your driving habits then the Root Car Insurance app will offer you different coverage packages for different prices.

How Much Can You Save?

Their website currently states that there is, “only one way to find out!” I love this because it is very true. You will never know how much money you can save with any insurance carrier until you get a quote, or in Root Car Insurance’s instance, until you try their app. They go on to state that customers have saved “52% or more” on their car insurance. An enormous figure, but not unreasonable. Just this week we saved a customer over $4,000 on their total insurance package. This included their auto, home, and umbrella coverage. They went from $8,200 to below $4,000. So it can happen – nothing new here.

Where is Root Car Insurance Available Currently

The app is available and live in many states including Maryland and Pennsylvania. I’m not sure of their intentions in other eastern states, but we will see as time goes on. They do recognize on the website that “each state is regulated differently” and they are trying to expand as fast as they can.

How Does Root Rate Drivers

The whole marketing focus of Root seems to be on how you drive. Their front page says it right there, “Get a rate based primarily on how you drive”. Primarily is a key word here because it means that it truly is only a fraction of the total rating calculation.

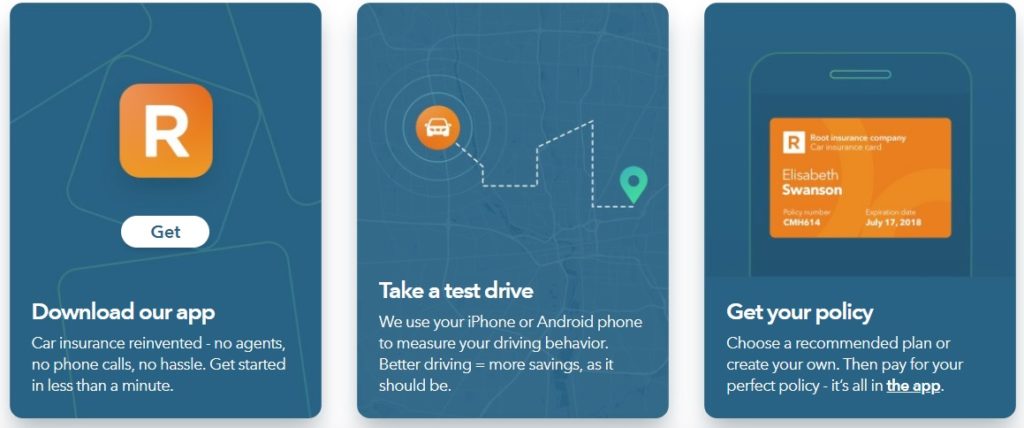

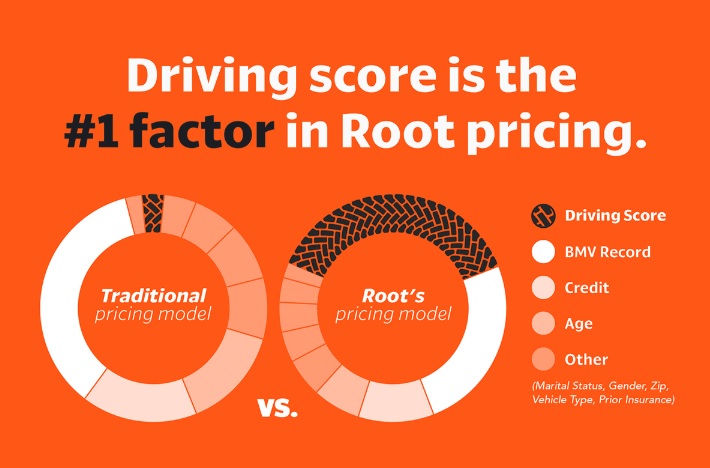

Root’s Rating Methodology

Here we have a breakdown of the rating considerations for the Root Car Insurance app. This graph highlights driving ability as the number one consideration with the BMV record in second. The BMV record is the driving history, or score, of the driver. Oftentimes this is the number one consideration for most car insurance carriers. So Root has stepped out on faith and inverted their calculations for pricing when compared to the conventional methodology.

Graph of Roots Rating Model Compared to a “Traditional Pricing Model”

I feel like this graph gives a more digestible illustration comparing the Root Car Insurance app’s pricing versus a traditional model. As you can see Root definitely takes the driving score into a higher consideration.

I do think the “traditional” model is a bit skewed. As time has progressed regular insurance companies do consider the driving score more and more. For instance, Nationwide will give a driver a huge discount if they demonstrate that they are safe drivers. Those discounts can range from 5-35%. That is a huge amount which is potentially comparable to Root’s pricing model, just taken from a different angles.

Opinions & Potential Problems

Adverse Selection

I applaud the Root Car Insurance app for attempting to take insurance into a new era. The biggest problem that I see ahead for them is adverse selection.

Adverse selection is a risk insurance companies tackle daily. A common example is a person purchasing life insurance claiming to be a non-smoker when in actuality they do smoke.

I believe because Root focuses on “driving ability” and less on driving history they have positioned themselves for an adverse selection scenario. High-risk drivers usually have high insurance costs, and that is a very purposeful. Now those high-risk drivers are often shoppers of insurance too. “Shoppers” is a term in the insurance industry that refers to individuals who jump from company to company seeking the lowest cost possible. Root seems like a perfect candidate for shoppers, but unfortunately they are often bad drivers. This adverse selection could be a big issue as claims arise and progress.

The Local Touch

Another disadvantage Root has is that they are 100% web based. They tout their app to be able to handle any scenario for customer service. If you get into a car accident and you have the Root Car Insurance app – then the app should be able to handle that. They also have a customer support team available 24/7 via email and they “do their darn best to return all emails within 24 hours”.

I see this as a huge issue. I can understand the reasoning behind creating an awesome app to handle it all. It helps on HR costs and therefore can hopefully decrease the insurance rates for their clients. I get it. It is a great idea but if someone gets into an accident – they want to talk to somebody – and better yet – somebody who they know and built a relationship with and can potentially see in person.

I utilize Google Trends often. When I type in Root Insurance into Google Trends the top inquiries are: “root insurance phone number” and “root insurance customer service number”. Although it is buried in their website, they do have an actual number and it is 18669809431. That is me doing my part to help all those google searchers looking for it.

Again, the Root Car Insurance App’s Customer Service Number is 18669809431

Final Thought

Like I state before, I applaud Root’s efforts and believe if they can overcome the adverse selection issue and maintain awesome customer service – then they have a shot.

If you would like to get a quote from a “traditional” car insurance company and build a relationship with a insurance professional then consider working with us. If you have any questions, want a quote, or free consultation, please give us a call at 4102623176 or fill out the form below.

Mike Nolan of Breathe 379 and Jesse Cunningham V of Mountain View Insurance Solutions

Breathe 379 – Edgewood Based Non-Profit

Mike Nolan of Breathe 379 came by the office to share their awesome mission. Breathe 379 is a non-profit based in Edgewood, Maryland off of Nuttal Avenue.

The mission is: Finding and meeting needs of families in our communities and beyond.

They do the annual Christmas Toy Drive and other events to directly benefit our local community

Give us a message or a call to see how you can be involved! **Ask about the 3/20 program!!! Visit their page at http://breathe379.com/ to learn more

We exceeded our goal and raised $1,000 to donate to the Harford County Public Library system. The money will used to purchase the complete Hugo Award Novel Winners collection since 1939. Thank you Harford County Public Library for being so easy to work with during this initiative! A special shout-out to the library’s purchaser Jennifer R!

AND because we exceeded our initial goal of $800 we will also be able to purchase some AWESOME Nebula Award Winning books.

Thank you to all of the businesses that stepped up to the plate:

THANK YOU AGAIN. Very cool to complete a cool project like this within 2 days. I think that is a testimony to how the local businesses of Harford County are willing to support lasting initiatives to better our community!

Will insurance ever be more than a “just in case” – one dimensional commodity? It is a tool that allows its users to leverage their money by placing it in a collective pool. If there is a large enough pool, then some predictions can be made with surprising accuracy. The most important predictions for the insurance carrier’s sake, are frequency and severity of future claims. They take their predictions, charge a fee, and provide their clientele coverage. That is how every insurance works but I’m curious if this is this where the function of insurance ends – a one dimensional, just in case coverage? Or is there another way to utilize the massive leverage that insurance affords? I would argue that certain insurances, such as car and home insurance, are one dimensional, and most likely will always be one dimensional. They are purchased with the hope to never use them – a coverage just in case something happens.

Now, what about

life insurance? This is where it gets interesting. Life insurance can be

one dimensional if used as a short-term solution. For instance, a 20-year life

insurance policy to pay off the mortgage just in case the owner passes away

prematurely. The owner may or may not survive the 20-year term, therefore it is

a policy just in case – still one dimensional.

Permanent Life Insurance

But what happens when a permanent life insurance policy is used? Permanent life

insurance is a catch all phrase for policies that are designed to last the

insureds lifetime, and more importantly, pay the benefits one day. Everyone has

a guaranteed mortality, so we’ve just identified a coverage that transcends the

typical “just in case something happens” into a “when this happens one day”

coverage.

Insurance provides massive leverage and when that leverage is coupled with a

guaranteed outcome such as death, it creates a very interesting combination. It

allows for families to build tax-free legacies to pass on to their heirs. It

enables individuals to create cash-value that they can borrow against in the

future, tax-free. What about the huge threat of long-term care costs on a

retiree’s plan? Add a chronic-illness provision to a policy to help hedge that

risk. What happens if the owner of the policy gets disabled and cannot

contribute to the plan? If the waiver of premium for disability provision was

added to the policy, then the insurance company would fund the premiums for the

owner, and the plan would continue. A properly designed, forward thinking,

permanent life insurance policy can be leveraged to hedge against many

different risks of life. There are no cookie-cutter solutions for anything in the

insurance industry and this holds true for life insurance as well. The key is

to identify a goal, recognize potential risks, and design a plan accordingly.

Jesse Cunningham V is the owner of Mountain View Insurance Solutions located in Bel Air, Maryland. Weekly articles and videos are posted on our social medias outlets for the community to be educated, entertained, and empowered. Mountain View Insurance Solutions, 900 South Main Street #104, Bel Air MD 21014

We are now members of Choose Civility, Harford County, MD!

This is an awesome program put on by the Harford County Public Library system promoting respect, restraint, and responsibility are we are proud to now be supporting members!