We put this infographic together for our Harford County insurance clients and anyone else who may be interested. Here are 9 ways to lower your car insurance. We are an independent insurance agency in Bel Air, Maryland and specialize in personal lines insurance.

I had the honor to be a guest on Akers Financial Group’s weekly radio show last week on 105.7.

Brian Akers CFP, the owner of Akers Financial Group located in Forest Hill, MD, was the host and we dove into the topic of “Protecting Your Wealth”.

It was my first time in the radio “world” so it was pretty intimidating but also extremely fun. I had a great time that day and I’m extremely appreciative of the opportunity.

00:00 This is planning with a purpose with your host Brian Akers, certified financial planner and founder of Akers financial group. Now bringing personal financial planning to the lives of our listeners and clients. One person at a time. Here’s Brian Akers.

00:18 Welcome to planning with a purpose. I’m Brian Akers, a certified financial planner and owner of Akers Financial Group. Today our topic is protecting your wealth and we brought in a special guest. His name is Jesse Cunningham from Mountain View Insurance. Good Morning Jesse. Good morning. Thanks for having me. Well Jesse is here but we’re not really here. It’s sort of a a recorded show that was done earlier in time so we are now into the future and you’re hearing this live which is exciting for both of us because we get to hear our show and not actually be there. That’s a long story I guess there I let Jesse, we welcome to the show like what we’re going to try to do here. Planning with a purpose today is talk about property and casualty insurance. Explain it, explain what the look for. Explain how to protect yourself and your family.

01:00 Absolutely.

01:01 This

is also a precursor for our expo. We have a retirement planning expo that’s

April 5th on a Friday. It’s in the afternoon from 12 to like seven. Now. Jesse

is one of our speakers. He’ll be speaking on this topic that day. That’s a very

important topic to protect our wealth from anything that could destroy our

future. And so we really want to make sure we cover things here and also on

that Friday. If you like it, if you want find out more information about

anything you hear today, you can call Akers financial group at one eight three

three AFGE team 1-833-AFG-TEAM. All right, Jesse, tell us about yourself.

01:37 Okay.

So Jesse Cunningham grew up in Harford County. When it’s to see Mr C you can

call it. I’m the fifth. Yeah. So, um, call me whatever you want. Um, grew up in

Harford County, went to Calvert Hall, after college, moved to Hawaii. Okay,

nice. Yeah, so this is where the name Mountain View Insurance came from. I met

my beautiful wife out there, had our first son. We lived off grid three Akers

of land, um, solar panels. The whole $50 a month was our expenses to run the

house cause all which, which island were you on? Big Island. Hilo side of

volcanoes. Volcano. Exactly. So technically I lived in Mountain View, which is

like volcano. Oh, nice. Nice. So with that we sold the property, came back to

Maryland, Harford county. Offices in Bel Air. Sure. Um, and we started a

business. That was our seed money. So today’s topic is on protecting your

wealth, right? So property and casualty, that means car, home, umbrella

insurance. Right, right. So I’m one of the weird ones out there that thinks

insurance is actually fun. So my goal is to make this fun today. Oh, Lord

02:41 I’m

sorry I shouldn’t say it that way. All right, so those driving, are you

properly insured? Don’t be scared as we’re driving or talking about basically,

right?

02:49 Nope.

There’s two camps in why you should have insurance. Okay. Constantly we are

being bombarded with the commodity of insurance.

02:59 Exactly right. Lizards, all kinds of animals, women,

03:02 we’ll

save you money now. 15 minutes or less, right? It’s all about a commodity. And

then there’s the other camp that has assets. And they need to protect them.

Absolutely. And that’s what we’re going to focus on. Yep. So imagine a castle,

we have the store house, we have the treasure in the store house. You help

people grow that treasure, right? Yup, sure. I try and I help people protect

that treasure. We have a wall, we have a moat. So that’s the basics of what

property and casualty is supposed to be. It’s not supposed to be a commodity.

It’s supposed to protect your assets.

03:33 All

right? So the idea is you take a look at what you own and you start with your net

worth. We call that a financial fingerprint, financial fingerprint to US is who

are you? What do you own? How do you allocate your thing? So you do the same

thing when it comes to what do they own? House wise, what do they own dog wise?

What the automobile, things like that.

03:52 Exactly.

So big question is how much insurance do I need? You’ve heard of the term

insurance poor? Yeah, right. Derogatory term for the insurance industry. But

first we’d have to figure out how much insurance we need and how we do that is

to figure out how much assets you have.

04:08 All

right, so net worth and net worth and net worth would be your assets.

Everything you have invested minus your debt, and that’s sort of a net worth.

04:16 Absolutely.

So we take those assets and we say, look, Mr and Mrs. Jones, you have $2

million we need to protect. How do we do this correctly and affordably? Right?

Oftentimes in our industry it’s opposite. They want to say, let’s do it

affordably and correctly is second to that.

04:32 I

want to pay this much money and then give me whatever coverage that that is.

Exactly. Or when a new client will come in with us, the way the relationship

works is this. When someone comes in for a financial review and we do our

financial design, we’re sitting down with those clients. And then as we get to

the property and casualty, they bring in their declaration pages, their quotes,

and it sort of talks about what they have coverage. And then we’re talking

about it has a financial planner, the overview of everything. We say, well in

this, this case here, it looks like you don’t have enough coverage. And that’s

because we’ve examined that net worth first. And then they really have never

thought about it.

05:06 Absolutely.

And it’s not the most exciting thing to, to look at your declarations page for

insurance, but I love that you pointed out to your clients lets audit it. Let’s

see what your, uh, your liability coverages are specifically. And is that

enough for your assets?

05:20 Right.

So if you’re playing along at home, you can get your insurance policy out and

something called a declaration page. It comes with your bill

05:27 comes,

it’s usually once a year, the declarations that will show all your coverages

and it usually has the bill with it.

05:33 Okay.

So we’re talking about a person, you said, Mr or Mrs. Jones, I believe, and

there are $2 million. Now let’s just walk through what, what you want to do

first, auto or home.

05:44 Let’s

do auto. It’s a really interesting thing because there’s not many products or

services that the government requires you to have,

05:50 right?

But, but they require auto insurance. That’s when the state of Maryland, what

are those limits?

05:56 Three

Oh, excuse me, 30,000 slash 60,000 okay. Okay. That’s bodily injury. So 30 60,

whenever they do that, 30 60 the 30 is what per person? Per Person and then 60

is aggregate. So per occurrence or per incident, that’s if you were to do

something bad, right? You’re driving your vehicle, you heard someone, right?

They see you. Yup. This is liability covers. This is what protects your assets.

This is the front line. And so that’s um, the liability coverage, those as

bodily injury and says 30 slash 60. I’m really gonna have any slashes there,

right? The Ken. And later in the show, I’d like to dive into an appropriate

amount to have, if you want to be qualified for an umbrella policy. So we’ll

get into that later. But then the third number, um, I believe Maryland State

minimums are 15,000. That’s for property damage.

06:48 Okay,

so that’s, you’re in your car, you have an accent, he hit someone, you go in

someone’s yard, tear up the yard, and that’s property. It is. And if I’m

driving on six 95 going home, I hit someone’s Mercedes. That’s property too.

Okay. So if you have $15,000, which is Maryland state minimum, and you hit a

$50,000 car, guess who’s making up the difference? Uh, you run. No don’t do

that. We did not endorse that in any way as a terrible joke. So a 30, 60, 15,

30 is covering the bodily injury of the person you hit 60 covers the rest of people

in the car aggregate and then 15 would cover the car. Uh, exactly what the

property, the telephone pole, you hit the car, you hit. Sure. Whatever that’s

on the Maryland minimum, the Maryland minimum would make her policy cheaper.

Absolutely. But is that coverage at all?

07:40 Right.

So here’s the interesting thing. You can call me and I can save you hundreds of

dollars off the bat. Right. I could cut all of your coverages down to nothing

and save money. Exactly. But what’s the point? If you have assets to protect,

that’s a terrible, terrible idea. Okay. Yeah. So what would dumb normal auto

insurance coverage be like? Look, what should somebody buy this? Generally?

It’s a good question. So there’s different stages in life. Okay. If we want to

focus on retirees and they can do all stages, but let’s do that retirees, then

we’ll do and work backwards. Dang. Can the know, do the people that have no

money? The people with kids. Perfect. Perfect. Um, okay. If you, you’re retired

250,000 slash 500,000 okay. That allows you to qualify for an umbrella policy.

Alrighty. Alright. And explain what umbrella that will go in that more later in

the show, but just basics of umbrella. Okay. Umbrella policy is a strictly

liability coverage policy. That’s, that’s what it does, right? If you get sued,

you’re underlying coverage. This is the technical term for your car insurance,

your home insurance. That’s underlying coverages. Okay. That’s the first line

of defense. If you get sued. Sure. If the lawsuit exceeds that amount, the

umbrella policy kicks into a million. All right, and that’s $1 million umbrella

and that’s baseline. There’s, I have a client who has a $6 million umbrella.

Right, so it all depends on your assets.

09:03 Absolutely.

Cause you want to protect the assets with an umbrella policy. Many people when

we have our events or our workshops are all around Maryland. What happens is

when they come in to see us, we find that they do not have umbrella policies at

all. They might have stayed very well and put million dollars, $3 million saved

and then you don’t have any umbrella insurance and then that’s just a big thing

we must fix. What I mean by that is you have to add that on. Now the umbrella

policy, we are going to cover that in greater detail towards the end of the

show, but right now on the auto, the coverage limits. So we had the retiree,

you’re picking it up because they’ve saved and grown their money. Sure. Let’s

go. Go to the middle. We’re talking about the family, younger family with kids.

We’re not going to talk about families with 16, 18 year olds because that’s,

that’s more difficult. But the, the younger family that has um, a lot of people

in the car, this, things like that. What kind of coverage that they look at?

10:00 Right.

So it’s an interesting question because the majority of your price for auto

insurance comes through the comprehensive and collision coverage. Okay, so

comprehensive and collision. Most people think of full coverage. That’s not a

real term, but that’s what most people think. If you hit a deer or you covered,

if you hit another car, is your car covered? That’s where the majority of the

price for policy is. Right? So if you look at your bill, they’ll say comp

comprehensive, that is covering what that is covering every. Another way to say

it is other than collision.

10:30 Okay,

so it’s comp is other than collision, does that mean so many dings, your

windshield, the deer on dog, somebody hit

10:37 check

tree falls on, yeah. Okay, got it. Yeah, but this is covering our car or

somebody else’s car. Your car, your car and then then collision covers my car

or out of context. So those two things are always covering your asset, your

car. Okay. Now my point is that’s the bulk of your premium of your payment.

Okay. You would be so surprised to increase your liability limits which we were

talking about earlier. That’s not a huge expense. Okay, so if you are wise, you

have a higher liability limit then what you may need technically right now

because guess what? When you go to change insurances in a year, two years,

three years, the new insurance company is going to say what prior liability

limits that you have. We want to know and if you had the high liability limits,

the new company is going to look at you favorably and guess what? Your price is

better. Okay. So this is kind of forward looking. So then they start a class

hue for pricing. Absolutely. Yeah.

11:32 All

right. We’ll talk about pricing a little bit later. I have a lot of questions on

pricing, but when it comes to the bulk of the policy, comprehensive and

collision. So if you’re driving a car that’s under 10 years old, you should

have comp and collision and then you have a decision on deductibles. Right?

11:50 Right.

And so one of your clients was in our office. Yep. Lovely people. All of your

clients are great. I know you must attract that. I don’t understand. But

they’re great people and I tried to check only good ones. Well they are

definitely good ones. And the gentleman said, I partially self insure and I get

that if you have the assets, you know liquid assets to to shell out $1,000

deductible, no problem. Yup. Do it.

12:13 Exactly

right. And so it’s part of a financial plan is to build your emergency fund.

You build that emergency fund with the purpose to have the cash to cover a, a

incident that might be a thousand or so since you’re not reporting any and

every ding.

12:28 Exactly.

Because if you report every dig, your price per month is going to go up and you

got to pay more than the long run. It’s going to be a lot was the ding becomes

at Dong is going to hit you really hard. It’s like a bell

12:39 fairly

loud. And so, so we have um, we have like in that case you’re talking about

yesterday, he has self insuring a little bit more, but having more cash in

there. That comprehensive and collision. If you have a say three or four

different cars you might insure for collision, the newer ones and then the ones

that are 10, 12, 15 years old that might have not much collision value.

12:59 That’s

exactly what happens. So they had four cars, there was a 15, and in 2010 they

had full cup, full coverage. Remember that’s not a real term. They had

comprehensive and collision on those. Sure, and they did not have those

coverages on the other two. Sure. He said, hey Jess, if I get into an accident,

it’s fine. I’ll just buy a new 1995 F150 foreign. Yeah.

13:19 All

right. Well Jesse, this has been a good good. The beginning of our talk about

property and casualty insurance, hopefully those out there listening or understanding

the basic concepts of auto and homeowners insurance that we’re trying to cover

today, but we’re also talking about our expo. We have coming April the fifth so

April the fifth is a Friday. We’re going to start around noon, come register,

get lunch. We also recommend that you register online@ Akersfinancial.com

you’ll see an expo tab on that tab. You’ll be able to see their speakers or

schedule and you can line up and sign up for each class. We highly recommend

that you sign up and preregister so that we can have everything prepared for

you and we can buy enough food for everybody. The day goes with classes at one,

two, three and four and five o’clock we have music and food, and six o’clock we

have a final speaker. He’ll talk about the stock market, so it’s a big day.

Jesse is one of our speakers that day. Today we’re covering more about auto and

homeowners. Then we’ll have more information about that after these messages.

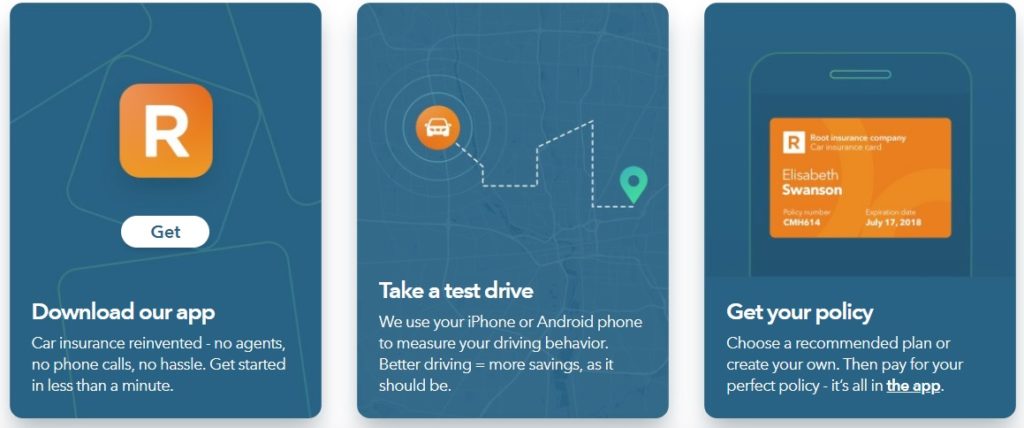

The latest craze going around Facebook and other media outlets – Root Car Insurance. The concept is fairly simple on the surface: download the app, root monitors how you drive, and eventually it will dictate a monthly price for your car insurance. Disclaimer: we do not offer Root Car Insurance. We are just making observations and opinions in this blog article.

Their website highlights “simple pricing, fair rates, and modern products”. As a insurance professional it is important to stay ahead of trends and understand the ever changing marketplace. I do believe there will be major disruption in the industry as time goes on, but is Root Car Insurance it? Let’s dive into some specifics of their offers before we make an opinion.

The first step to working with Root Car Insurance is to download their app on either the iPhone or Android. It is compatible with both operating systems which is very convenient. Currently the app is available on iPhone 5s and above and “most” androids.

2. Drive!

Once you have downloaded the application then its time to drive. They will monitor your driving behavior such as speed, braking, what time of the day you drive, where you drive, etc. This is not a new phenomenon in the insurance industry as the majority of insurance companies now offer plug-in devices or apps to just this.

3. Choose your plan

After a sufficient amount of data has been collected on your driving habits then the Root Car Insurance app will offer you different coverage packages for different prices.

How Much Can You Save?

Their website currently states that there is, “only one way to find out!” I love this because it is very true. You will never know how much money you can save with any insurance carrier until you get a quote, or in Root Car Insurance’s instance, until you try their app. They go on to state that customers have saved “52% or more” on their car insurance. An enormous figure, but not unreasonable. Just this week we saved a customer over $4,000 on their total insurance package. This included their auto, home, and umbrella coverage. They went from $8,200 to below $4,000. So it can happen – nothing new here.

Where is Root Car Insurance Available Currently

The app is available and live in many states including Maryland and Pennsylvania. I’m not sure of their intentions in other eastern states, but we will see as time goes on. They do recognize on the website that “each state is regulated differently” and they are trying to expand as fast as they can.

How Does Root Rate Drivers

The whole marketing focus of Root seems to be on how you drive. Their front page says it right there, “Get a rate based primarily on how you drive”. Primarily is a key word here because it means that it truly is only a fraction of the total rating calculation.

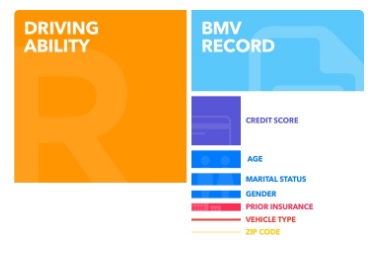

Root’s Rating Methodology

Here we have a breakdown of the rating considerations for the Root Car Insurance app. This graph highlights driving ability as the number one consideration with the BMV record in second. The BMV record is the driving history, or score, of the driver. Oftentimes this is the number one consideration for most car insurance carriers. So Root has stepped out on faith and inverted their calculations for pricing when compared to the conventional methodology.

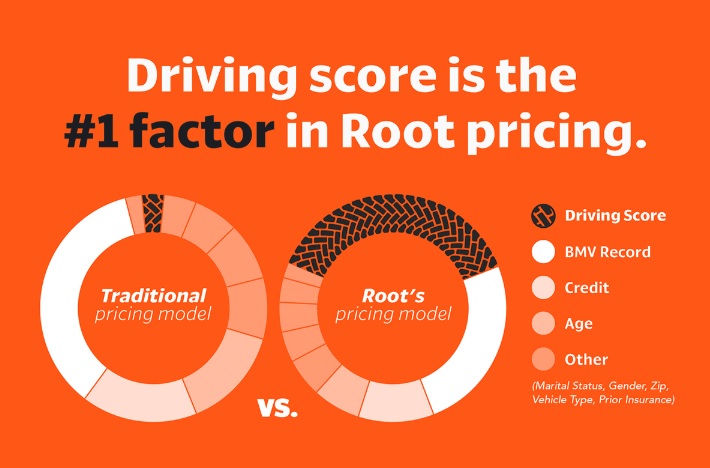

Graph of Roots Rating Model Compared to a “Traditional Pricing Model”

I feel like this graph gives a more digestible illustration comparing the Root Car Insurance app’s pricing versus a traditional model. As you can see Root definitely takes the driving score into a higher consideration.

I do think the “traditional” model is a bit skewed. As time has progressed regular insurance companies do consider the driving score more and more. For instance, Nationwide will give a driver a huge discount if they demonstrate that they are safe drivers. Those discounts can range from 5-35%. That is a huge amount which is potentially comparable to Root’s pricing model, just taken from a different angles.

Opinions & Potential Problems

Adverse Selection

I applaud the Root Car Insurance app for attempting to take insurance into a new era. The biggest problem that I see ahead for them is adverse selection.

Adverse selection is a risk insurance companies tackle daily. A common example is a person purchasing life insurance claiming to be a non-smoker when in actuality they do smoke.

I believe because Root focuses on “driving ability” and less on driving history they have positioned themselves for an adverse selection scenario. High-risk drivers usually have high insurance costs, and that is a very purposeful. Now those high-risk drivers are often shoppers of insurance too. “Shoppers” is a term in the insurance industry that refers to individuals who jump from company to company seeking the lowest cost possible. Root seems like a perfect candidate for shoppers, but unfortunately they are often bad drivers. This adverse selection could be a big issue as claims arise and progress.

The Local Touch

Another disadvantage Root has is that they are 100% web based. They tout their app to be able to handle any scenario for customer service. If you get into a car accident and you have the Root Car Insurance app – then the app should be able to handle that. They also have a customer support team available 24/7 via email and they “do their darn best to return all emails within 24 hours”.

I see this as a huge issue. I can understand the reasoning behind creating an awesome app to handle it all. It helps on HR costs and therefore can hopefully decrease the insurance rates for their clients. I get it. It is a great idea but if someone gets into an accident – they want to talk to somebody – and better yet – somebody who they know and built a relationship with and can potentially see in person.

I utilize Google Trends often. When I type in Root Insurance into Google Trends the top inquiries are: “root insurance phone number” and “root insurance customer service number”. Although it is buried in their website, they do have an actual number and it is 18669809431. That is me doing my part to help all those google searchers looking for it.

Again, the Root Car Insurance App’s Customer Service Number is 18669809431

Final Thought

Like I state before, I applaud Root’s efforts and believe if they can overcome the adverse selection issue and maintain awesome customer service – then they have a shot.

If you would like to get a quote from a “traditional” car insurance company and build a relationship with a insurance professional then consider working with us. If you have any questions, want a quote, or free consultation, please give us a call at 4102623176 or fill out the form below.